Understanding FC Personal Loan Top Up Eligibility: A Comprehensive Guide

Personal loans have become a vital financial resource for many individuals seeking to cover various expenses, be it for education, medical emergencies, or home improvements. However, there are times when the initial loan amount may not suffice, and this is where the concept of a personal loan top-up comes into play. The term "FC Personal Loan Top Up Eligibility" refers to the criteria and conditions that borrowers must meet to qualify for an additional loan amount on top of their existing personal loan with the financial institution, FC.

Understanding the eligibility criteria for a personal loan top-up is crucial for borrowers who wish to enhance their financial capacity without undergoing the entire loan application process again. This comprehensive guide aims to delve into the various aspects of FC Personal Loan Top Up Eligibility, providing you with a clear understanding of what it entails and how you can benefit from it. By exploring factors such as credit score requirements, repayment history, and other financial conditions, you'll be better equipped to assess your eligibility for a loan top-up.

Whether you're looking to finance a new project or consolidate existing debts, knowing the ins and outs of FC Personal Loan Top Up Eligibility can provide you with the financial flexibility you need. With this guide, we aim to provide you with valuable insights and actionable information, helping you navigate the process with ease and confidence. Let's explore the world of personal loan top-ups and unlock the potential benefits it holds for you.

- What The Perverse Family Hid Leaked Sex Scandal Rocks Community

- Gretchen Corbetts Secret Sex Scandal Exposed The Full Story

- Walken Walken

Table of Contents

- Understanding Personal Loans

- What is a Personal Loan Top Up?

- Eligibility Criteria for FC Personal Loan Top Up

- Credit Score and Its Importance

- Repayment History and Its Impact

- Income Stability and Assessment

- Employment Status and Its Role

- Debt-to-Income Ratio

- Documentation Required

- Benefits of Personal Loan Top Up

- Potential Risks and Considerations

- How to Apply for FC Personal Loan Top Up

- Frequently Asked Questions

- Conclusion

Understanding Personal Loans

Personal loans are unsecured loans that individuals can obtain from financial institutions without the need for collateral. They are typically used for personal expenses such as consolidating debt, financing home renovations, or covering emergency situations. Unlike secured loans, personal loans rely heavily on the borrower's creditworthiness, which includes factors such as credit score, income stability, and repayment history.

Financial institutions assess the risk involved in lending money without collateral, and as a result, they set specific interest rates and repayment terms based on the borrower's profile. Understanding the dynamics of personal loans is essential for borrowers looking to leverage them effectively for their financial needs.

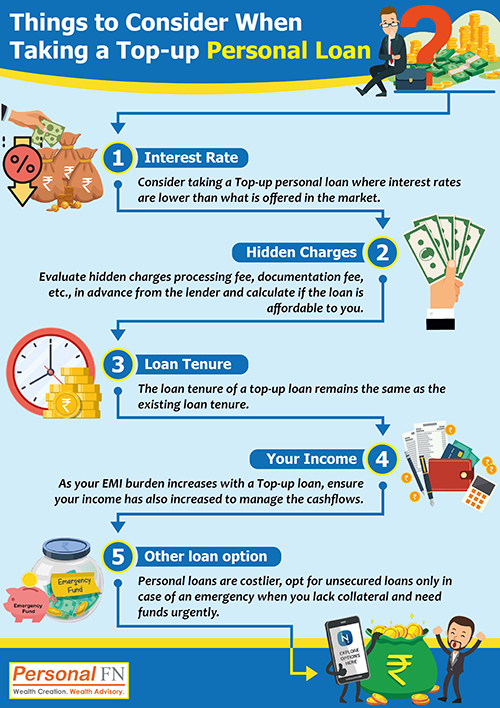

What is a Personal Loan Top Up?

A personal loan top-up is an additional loan amount that borrowers can avail of on their existing personal loan. It provides an opportunity for borrowers to access more funds without undergoing the full loan application process. This feature is particularly beneficial for those who have established a good repayment history with their lender, as it allows for a quicker and more convenient access to additional funds.

- Sky Bri Leak

- Tennis Community Reels From Eugenie Bouchards Pornographic Video Scandal

- Peitners Shocking Leak What Theyre Hiding From You

The top-up amount is usually added to the outstanding balance of the existing loan, and the terms and conditions, including interest rates and repayment schedules, are often adjusted to accommodate the new loan amount. Borrowers can use the top-up for various purposes, such as funding new projects, managing unexpected expenses, or even consolidating other debts for better financial management.

Eligibility Criteria for FC Personal Loan Top Up

When it comes to FC Personal Loan Top Up Eligibility, specific criteria must be met to qualify for the additional loan amount. Understanding these criteria is crucial for borrowers who wish to apply for a top-up with FC. Here are some key factors that determine eligibility:

- Credit Score: A good credit score is essential for qualifying for a personal loan top-up. It reflects the borrower's creditworthiness and ability to repay the loan.

- Repayment History: Consistent and timely repayment of the existing loan is a positive indicator for lenders, as it demonstrates financial responsibility.

- Income Stability: Lenders assess the borrower's income stability to ensure that they can handle the additional financial burden of a top-up loan.

- Employment Status: Steady employment and a reliable source of income are important factors in determining eligibility for a loan top-up.

- Debt-to-Income Ratio: A manageable debt-to-income ratio indicates that the borrower can afford to take on additional debt without financial strain.

Meeting these criteria increases the likelihood of being approved for a personal loan top-up with FC, allowing borrowers to access the funds they need with ease.

Credit Score and Its Importance

The credit score is a numerical representation of a borrower's creditworthiness, based on their credit history and financial behavior. It plays a vital role in determining eligibility for loans, including personal loan top-ups. A high credit score indicates a strong financial profile and increases the chances of approval, while a low score may result in higher interest rates or even denial of the loan.

Lenders rely on credit scores to assess the risk involved in lending money to a borrower. A good credit score not only improves the chances of qualifying for a loan top-up but also influences the terms and conditions of the loan, such as interest rates and repayment schedules. Borrowers with excellent credit scores may benefit from lower interest rates, making the loan more affordable.

Repayment History and Its Impact

Repayment history is a record of how a borrower has managed their previous loan obligations. It includes information on timely payments, missed payments, and any defaults or delinquencies. A positive repayment history is a strong indicator of a borrower's financial responsibility and reliability.

Lenders consider repayment history when assessing eligibility for a personal loan top-up. Borrowers who have consistently made timely payments on their existing loans are more likely to be approved for a top-up, as they demonstrate a commitment to meeting their financial obligations. Conversely, a poor repayment history may hinder the chances of approval and result in less favorable loan terms.

Income Stability and Assessment

Income stability is a crucial factor in determining eligibility for a personal loan top-up. Lenders assess the borrower's income to ensure that they have a reliable and steady source of funds to repay the additional loan amount. A stable income indicates financial security and the ability to manage increased financial responsibilities.

Borrowers with a consistent income stream are viewed more favorably by lenders, as they pose a lower risk of default. Lenders may also consider additional sources of income, such as rental income or investment returns, to evaluate the borrower's overall financial health. It's essential for borrowers to provide accurate and comprehensive income documentation to support their loan application.

Employment Status and Its Role

Employment status is a significant factor in determining eligibility for a personal loan top-up. Lenders prefer borrowers with stable employment and a steady job history, as it reflects financial stability and the ability to repay the loan. Borrowers with long-term employment in reputable organizations are often seen as lower risk, increasing their chances of loan approval.

Self-employed individuals or those with irregular income may face more scrutiny during the loan assessment process. However, providing additional documentation, such as business financial statements or tax returns, can help demonstrate financial stability and enhance eligibility for a personal loan top-up.

Debt-to-Income Ratio

The debt-to-income (DTI) ratio is a measure of a borrower's total monthly debt obligations compared to their monthly income. Lenders use the DTI ratio to assess a borrower's ability to manage additional debt. A lower DTI ratio indicates that the borrower has a manageable level of debt relative to their income, making them a suitable candidate for a personal loan top-up.

To calculate the DTI ratio, divide the total monthly debt payments by the gross monthly income and multiply by 100 to get a percentage. A DTI ratio of 36% or lower is generally considered favorable by lenders. Borrowers with a high DTI ratio may need to improve their financial situation by paying down existing debts before applying for a top-up loan.

Documentation Required

When applying for a personal loan top-up, borrowers must provide specific documentation to support their application. The documentation helps lenders verify the borrower's financial situation and assess their eligibility for the loan. Commonly required documents include:

- Proof of identity (e.g., passport, driver's license)

- Proof of address (e.g., utility bill, rental agreement)

- Income proof (e.g., salary slips, bank statements)

- Employment details (e.g., employment letter, business registration for self-employed)

- Existing loan details (e.g., loan statement, repayment history)

Providing accurate and complete documentation is crucial for a smooth loan application process. Borrowers should ensure that all documents are up-to-date and readily available to avoid delays in the approval process.

Benefits of Personal Loan Top Up

Opting for a personal loan top-up offers several advantages for borrowers seeking additional funds. Some of the key benefits include:

- Convenience: Borrowers can access additional funds without undergoing a new loan application process, saving time and effort.

- Flexibility: The top-up amount can be used for various purposes, such as home renovations, debt consolidation, or unexpected expenses.

- Competitive Interest Rates: Borrowers with a good credit history may benefit from lower interest rates on the top-up loan, reducing the overall cost of borrowing.

- Improved Financial Management: Consolidating multiple debts into a single loan can simplify financial management and reduce the burden of keeping track of multiple payments.

- Extended Repayment Terms: The repayment terms for the top-up loan may be adjusted to accommodate the borrower's financial situation, providing more flexibility in managing monthly payments.

Potential Risks and Considerations

While a personal loan top-up offers numerous benefits, borrowers should also be aware of potential risks and considerations before proceeding. Some key factors to keep in mind include:

- Increased Debt Burden: Taking on additional debt can strain the borrower's finances, especially if they are already managing multiple financial obligations.

- Higher Interest Costs: Depending on the borrower's credit profile and market conditions, the interest rate on the top-up loan may be higher than the original loan.

- Impact on Credit Score: Applying for a top-up loan may result in a hard inquiry on the borrower's credit report, temporarily affecting their credit score.

- Repayment Challenges: Borrowers should carefully assess their ability to manage the increased monthly payments to avoid defaulting on the loan.

How to Apply for FC Personal Loan Top Up

Applying for an FC personal loan top-up involves several steps to ensure a smooth and efficient process. Here's a step-by-step guide to help you apply for a personal loan top-up with FC:

- Assess Your Eligibility: Before applying, review the eligibility criteria, including credit score, repayment history, income stability, and debt-to-income ratio, to determine your suitability for a top-up loan.

- Gather Required Documentation: Collect all necessary documents, such as proof of identity, address, income, employment, and existing loan details, to support your application.

- Contact FC: Reach out to FC through their official website, customer service hotline, or visit a branch to inquire about the top-up loan application process.

- Submit Your Application: Complete the loan application form and submit it along with the required documentation to FC for review.

- Await Approval: FC will assess your application and conduct a credit evaluation to determine your eligibility for the top-up loan. This process may take a few days.

- Review Loan Offer: Once approved, review the loan offer, including interest rates, repayment terms, and any associated fees, before accepting the terms.

- Accept the Loan Offer: If you agree with the loan terms, sign the loan agreement and proceed with the disbursement of the top-up amount.

By following these steps, you can successfully apply for an FC personal loan top-up and access the additional funds you need for your financial goals.

Frequently Asked Questions

Q1: What is the minimum credit score required for an FC personal loan top-up?

A1: The minimum credit score requirement varies, but generally, a score of 650 or above is considered favorable for a personal loan top-up.

Q2: Can I apply for an FC personal loan top-up if I have an existing loan with a different lender?

A2: Typically, FC offers top-up loans to existing customers. However, you may need to consolidate your existing loan with FC to qualify for a top-up.

Q3: How long does it take to get approval for an FC personal loan top-up?

A3: The approval process may take a few days, depending on the completeness of the application and documentation provided.

Q4: Is there a maximum limit on the top-up amount I can receive?

A4: Yes, the top-up amount is subject to the lender's policies and the borrower's credit profile and repayment capacity.

Q5: Will applying for a top-up loan affect my credit score?

A5: Yes, applying for a top-up loan may result in a hard inquiry, which can temporarily impact your credit score.

Q6: Can I use the top-up amount for any purpose?

A6: Yes, the top-up amount can be used for various purposes, such as home improvements, debt consolidation, or emergency expenses.

Conclusion

Understanding FC Personal Loan Top Up Eligibility is crucial for borrowers seeking additional funds to meet their financial needs. By evaluating key factors such as credit score, repayment history, and income stability, borrowers can assess their suitability for a top-up loan with FC. The convenience, flexibility, and potential benefits of a personal loan top-up make it an attractive option for managing financial obligations and achieving personal goals.

However, borrowers should also be mindful of potential risks and carefully consider their ability to manage increased debt before proceeding. With the right preparation and understanding of the eligibility criteria, borrowers can navigate the process with confidence and secure the financial support they need.

For more information on personal loan top-ups and financial advice, consider visiting reputable financial websites or consulting with a financial advisor to make informed decisions.

This HTML-formatted content provides a comprehensive guide on FC Personal Loan Top Up Eligibility, covering all necessary aspects, including eligibility criteria, benefits, risks, and the application process. It is structured to be informative, engaging, and accessible to a broad audience.